Danmarks Nationalbank has published a paper about cash use in Denmark 1. The paper draws on the results of the latest survey of citizens’ payment habits, which took place in the autumn of 2025 – the latest in a series that started in 2017.

Respondents completed a payment diary with their payments over one full day. In addition, they answered a number of questions about payment preferences and cash, for example their preferred payment solutions and their views on shops’ obligation to accept cash.

The survey is particularly important given that:

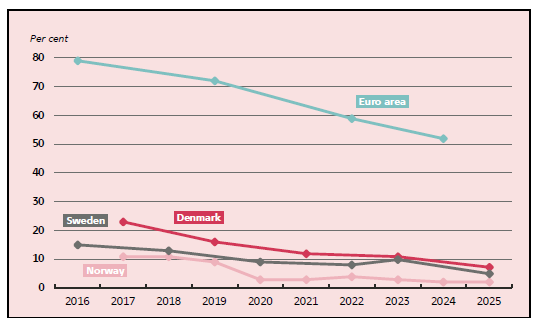

Internationally, the Nordic countries, including Denmark, have the lowest use of cash, although this remains slightly higher in Denmark than in the other Nordic countries. In Norway, there are also rules regulating the use of cash in shops, but in Sweden there is no general obligation to accept cash.

Apart from this slightly higher figure, there is little evidence that Denmark’s obligation to accept cash – which means that, as a rule, businesses must accept cash – is making a difference (see page 4). The declining use of cash is not a reflection of fewer shops accepting cash, but rather that fewer Danish citizens prefer to pay with cash.

Source: Danmarks Nationalbank, ECB, Norges Bank and Sveriges Riksbank.

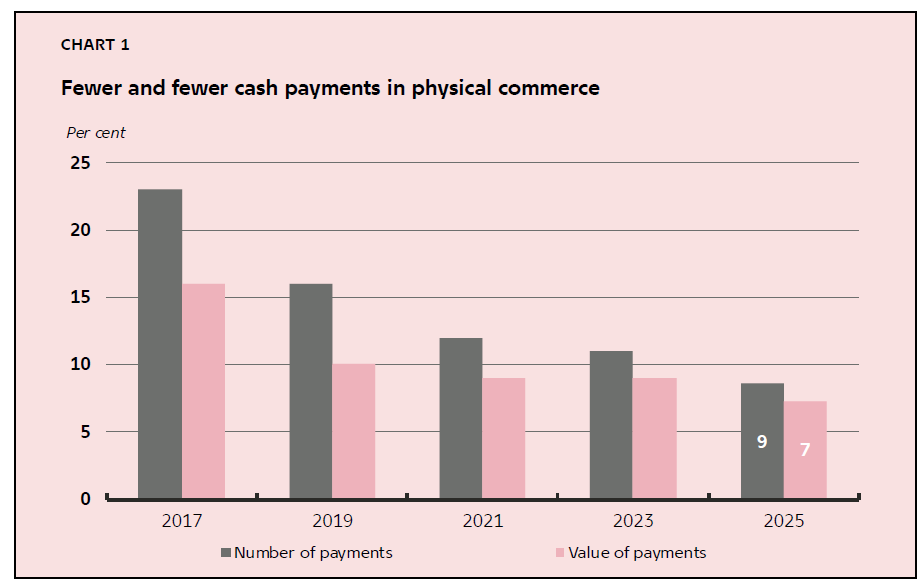

The number of payments in physical commerce is declining as more payments take place both in online trade and via apps in physical commerce. Within this broader trend, the use of cash for payments has also been declining for a number of years, and there are no signs that this trend is slowing. Danes have been willing to adopt new card and mobile payment solutions as they have been introduced.

Cash was used in 9% of payments in physical commerce in 2025 and accounts for 7% of the total value of payments in physical commerce.

Use of cash for the purchase of groceries has fallen from 30% in 2019 to 13% today. This figures still makes up more than half of all cash payments in physical commerce, but even here cash is also being used less.

Perhaps with an eye to Sweden, where cash decline has been linked to cash recalls, this analysis considers what has happened in Denmark.

The paper found that the recall of the 1,000 krone banknote and the invalidation of banknotes from series issued prior to 2009 as legal tender, announced in November 2023 and taking effect after 31 May 2025, led to a decline in cash in circulation, as circulation of other banknotes has not increased correspondingly.

The total circulation of banknotes and coins amounted to approximately 1.7% of GDP in 2025, compared with around 2.6% in 2023. Circulation of the 500 krone banknote has risen only slightly since the start of the recall. This suggests that there has been relatively little substitution between the two denominations.

However, the recall has not affected the size of cash payments in physical commerce. The average cash payment has thus only declined marginally, from DKK 245 in 2023 to DKK 242 in 2025.

Older citizens are increasingly choosing to pay using digital payment solutions, narrowing the gap in the use of cash across age groups. Since 2017, Danish citizens over the age of 70 have reduced their use of cash from 40% of payments to 14% in 2025.

Cash is being used less frequently in person-to-person (P2P) payments. From 2023 to 2025, the share of payments made in cash almost halved, so that in 2025 cash payments accounted for approximately one in eight payments between Danish citizens. While this is part of a general decline in P2P payments across payment solutions, the cash decline is greater than the trend.

One risk highlighted is that the decline in the use of cash in physical commerce may also imply that Danish citizens are less willing to accept cash and it may be perceived as less practical, for example because it takes time to deposit it into a bank account via an ATM. A self-reinforcing development may therefore arise.

Between 2023 and 2025, those who stated that it would be a problem for them if there were no cash in society in ten years time rose from about 37% to 58%, even while there has been a decline in the use of cash.

The share of Danish citizens who believe that all shops should be obliged to accept cash has increased from 38% to 44%. The share of people saying they don’t want a society without cash because cash is important has more than doubled since 2023.

An increased focus on cash as a contingency measure has led to the share of Danish citizens holding more than DKK 1,000 in cash rising from 33% in 2023 to 41%.

Since 2023, the banks have reduced the total number of ATMs by 24% and at the same time a larger share of the remaining ATMs are concentrated among a smaller number of specialised operators. In 2024 Danske Bank sold its 177 ATMs to the cash handling company Nokas. Nokas also handles technical operation and cash handling for KONTANTEN, a joint network of ATMs linked to a number of Danish banks.

Interestingly the distance to ATMs is estimated to be unchanged despite fewer ATMs. It is estimated that 1% of Danish citizens live more than 10km from their nearest ATM, a figure that is largely unchanged compared with 2023.

The number of ATMs with deposit functionality has also declined in recent years. The potential importance of this is increased because depositing cash generally requires that one is a customer of the bank that owns the ATM, unless banks cooperate, for example through KONTANTEN. The closure of a single ATM with deposit functionality can therefore have a greater impact on access to cash deposits than the closure of an ATM with withdrawal functionality has on access to withdraw cash.

Given that the launch of the new series will require citizens to return their 2009 series notes, it is important that the infrastructure to do this is in place.

You could almost describe Denmark as a ‘post-cash’ society. Despite long standing cash acceptance regulations, the elderly are learning to pay digitally, the banks have virtually exited the cash business, the payment industry and government have worked together so that card payments are usable in a crisis etc.

At the same time the population store cash and value cash to the extent that a new banknote series is to be issued. This report lays out the paradox and dichotomy that this reality presents to the Nationalbank and Danish society.

In Denmark there is a statutory cash rule which means that payment recipients in physical commerce must, as a general rule, accept cash during the daytime, unless the exceptions in the Payments Act apply. The exceptions include remote commerce, including online trade and self-service environments, as well as payments in cash from other businesses. Staffed shops are also not required to accept cash between 10pm and 6am, and in areas with an increased risk of robbery, the obligation to accept cash does not apply from 8pm.

Danish legislation also contains a number of provisions that limit the use of cash due to costs associated with cash handling, risks of money laundering, undeclared work and tax evasion. This applies whether the payment is made in a single transaction or as several transactions that appear to be interconnected.

The use of cash is also restricted under the Danish Coinage Act, as no payees are obliged to accept more than 25 coins of any denomination in a single payment.

Unusually, the report is clear that cash cannot stand alone as a payment contingency measure at a societal level, among other things because it has to be available in advance, and because in a crisis situation practical challenges will arise in handling large volumes of cash, including with regard to change and the storage of larger cash reserves in shops, as well as the transport of cash to and from shops, banks, ATMs, etc.

In Denmark payment cards are the primary payment contingency measure. Card payment contingency measures have already been established in most nationwide grocery chains. This is being extended so that by the third quarter of 2026 it will include all pharmacies.

It is possible to make offline payments for at least one week, both with physical payment cards and wallets on mobile phones, for example Apple Pay or Google Pay, using a Danish-issued payment card from Dankort, Mastercard or Visa.

In addition, offline card payments using physical payment cards and a PIN code are already a widespread solution in retail trade when the internet is not working or when there are outages in the card payment infrastructure.

1 - ANALYSIS | Payments 26 June 2026 | No. 13. Ditte Johanne Jensen, Retail Payments Expert and Lasse Holm Hélinck, Principal Economist.