Technological innovation is advancing at a pace that is transforming how societies pay, transact, and interact. Changes that once unfolded over decades now occur within years, fundamentally redefining the role and nature of money. As reflected in our new white paper ‘Currency Fast Forward – Future Developments of the Currency Cycle’ , one insight stands above all: the future of money will not be determined by a choice between physical and digital forms, but by their ability to coexist and reinforce one another. Across all regions, whether they rely heavily on cash, have advanced digital payment systems, or face the cash paradox of declining usage yet rising circulation, public money remains essential. It continues to serve as an anchor of trust, inclusion, and resilience.

The dual structure of public and private money is essential to the stability of the monetary system. Public money, issued by central banks, provides reliability and serves as the reference point for all private forms of money. Private money fuels innovation and convenience, but its credibility depends entirely on its convertibility into public money. Weakening the public cash cycle ultimately weakens trust in the entire ecosystem.

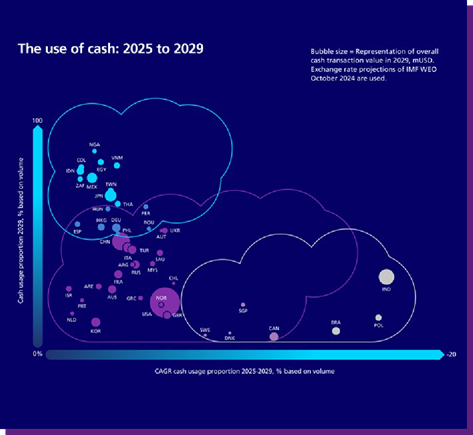

This dynamic is visible across high-volume cash economies, where cash is indispensable; across cash paradox markets such as the US and eurozone, where cash in circulation keeps growing; and across cash-decline countries like Sweden, where the retreat from cash has exposed vulnerabilities when crises suddenly increase demand. In every case, a functioning cash cycle remains essential for national preparedness and financial stability.

According to our white paper, 45% of central banks anticipate a 5-10% increase in cash circulation by 2029, despite decreasing Point-of-Sale usage. The cash paradox is projected to expand as more countries show high circulation but low usage. While digital payments will grow, cash will remain relevant worldwide, supported by strong infrastructure and its role in trust, resilience, and financial inclusion. These forecasts exclude potential geopolitical or economic shocks, which could significantly shift future trends.

The interplay of accessibility and availability, underpinned by efficient, widely accepted payment infrastructure, shapes how cash functions in daily life. Affection for cash and trust in its authenticity further reinforce its role in everyday transactions.

Technology plays a crucial role in future-proofing the cash cycle by strengthening and modernizing it. Artificial intelligence is already transforming currency management. It enables more accurate forecasting, optimizes cash routing, and supports smarter lifecycle decisions that extend banknote lifespans.

Increased transparency through smart safes, local cash cycles, and data driven liquidity tools improves planning without compromising privacy. At the same time, the rise of logistical and digital standards is reducing complexity and costs, similar to how containerization revolutionized global shipping.

Central banks are reinforcing this modernized cash cycle through investments in infrastructure, stronger banknote security features, and public awareness initiatives. They are also supporting it with legislative measures that protect payment choice and with clearer crisis preparedness frameworks.

Protecting cash is increasingly recognized as protecting sovereignty and societal resilience. According to our survey, 36% of stakeholders identify national security and resilience as their top priority.

The same complementary logic applies to CBDCs. In our white paper, 83% of central banks support developing CBDCs alongside cash, viewing them as a natural digital extension of public money. A well designed CBDC can strengthen monetary sovereignty, broaden inclusion, and enhance resilience, particularly through offline capability, while preserving core public money attributes.

The most transformative development emerging from our research is the shift toward a holistic currency cycle. Instead of viewing physical and digital currency as separate or competing systems, central banks can consider them as a single interoperable ecosystem.

In this model, physical and digital public money, ie. a central bank digital currency, strengthen each other. One interoperable currency cycle strengthens the sovereignty of the national currency and enhances operational efficiency. It also improves clarity for users and ensures that public money remains accessible in all circumstances: online and offline, in everyday life and in times of crisis.

The path forward is unmistakably hybrid. A future that relies exclusively on digital systems risks exclusion and fragility; a future that clings only to cash misses the opportunities of innovation. Central banks are uniquely positioned to lead this balancing act. By securing robust cash infrastructures while simultaneously designing trusted digital complements, they can ensure that public money remains a pillar of stability and inclusion.

Cash and CBDC together will provide the resilience, sovereignty, and accessibility that societies will increasingly depend on. The future of money is hybrid – and shaping it responsibly is within our reach.