A new paper from the Federal Reserve Bank of Atlanta seeks to understand whether, how and to what extent merchants in the US influence consumers’ payment choices1. Using the 2024 Survey and Diary of Consumer Payment Choice, which recorded stated preferred payment methods and then actual choices at the point-of-sale (POS), the authors analysed why consumers sometimes deviate from their preferred option.

The context for the paper is a recent settlement between credit card networks and merchants. One consequence of the settlement is that merchants may look to use surcharges to guide consumers away from using premium credit cards that charge them high fees.

Even before the settlement, there have been stories about and survey evidence of merchants using discounts on cash purchases and surcharges on credit card purchases to try to influence consumers’ payment choice.

1.Most of the time, consumers use their preferred payment method for in-person purchases: 52.5% of in-person purchases for consumers who prefer using cash, 64.1% for debit-card-preferring consumers, and 72.8% for credit-card-preferring consumers.

Low-income, less educated, male, and unemployed consumers tend to prefer using cash. Higher-income, more educated, Asian, and retired consumers prefer credit cards.

2.Merchants’ refusal to accept payment methods is not the major reason consumers deviate from their preferences. However, lack of acceptance does play a role. For example, 22.4% of consumers who prefer using credit cards paid cash and reported that the merchant did not accept cards. By contrast, consumers who prefer to use cash made only 6.8% of their purchases with cards when cash was not accepted.

3.Petrol stations and food/beverage establishments are more likely than other merchants to impose surcharges on credit card purchases. Large-value purchases are more likely than smaller-value purchases to include discounts when they are paid for with cash.

4.Consumers are less likely to shift from using cards to using cash for large-value transactions and for purchases at petrol stations, grocery and convenience stores, and other food establishments. Older consumers, low-income consumers, and Black consumers are more likely to shift from using cash.

5.Consumers who prefer using cards are 13% less likely to shift to cash if the merchant accepts cards. Lack of card acceptance accounts for some cases in which consumers shift to cash. Offers of discounts for cash payments do not affect the probability of consumers who prefer cards switching to cash.

6.Consumers are less likely to deviate from using cards for large-value transactions

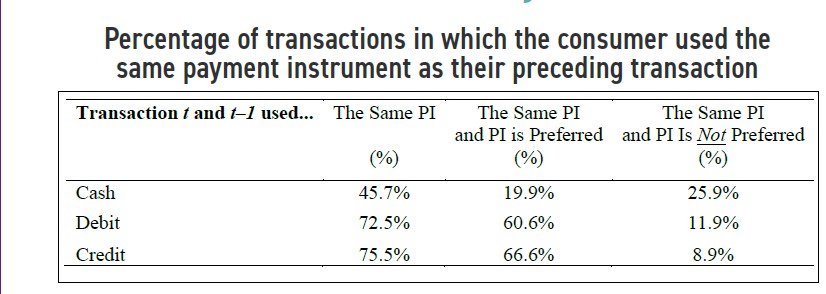

7.Inertia effects: consumers are more likely to use the same payment method for consecutive purchases. Inertia effects are stronger for debit and credit card purchases than for cash purchases.

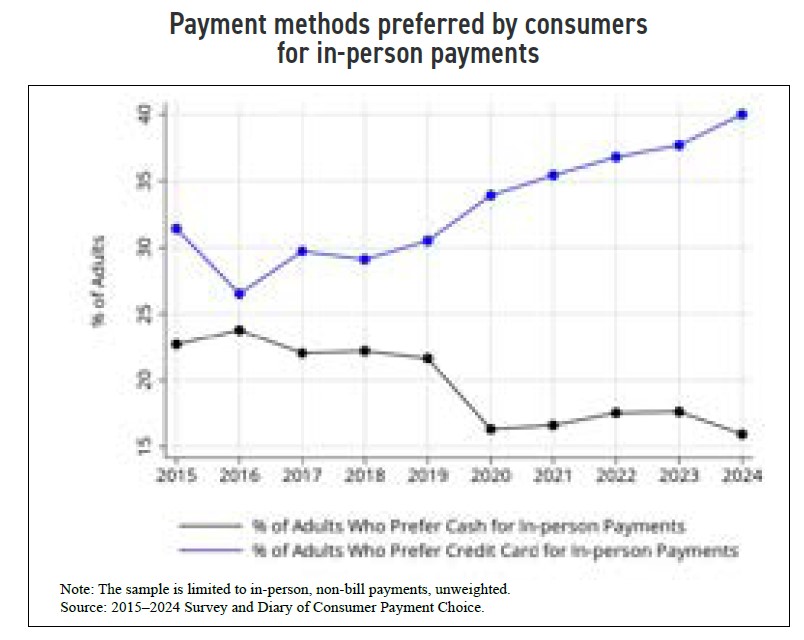

In 2024, 16% of consumers stated a preference for cash, 40% for debit cards, and 40% for credit cards.

Due to interchange fees charged by card issuers, credit card payments are more expensive for merchants to accept than debit card payments, and debit card payments are more expensive than cash payments. However, merchant steering is rare in the US.

Some reasons for changing how people pay are practical for both consumers and merchants – they don’t have enough cash on them, the transaction value is too low (or high), there is a discount or surcharge, the payment method is not available etc.

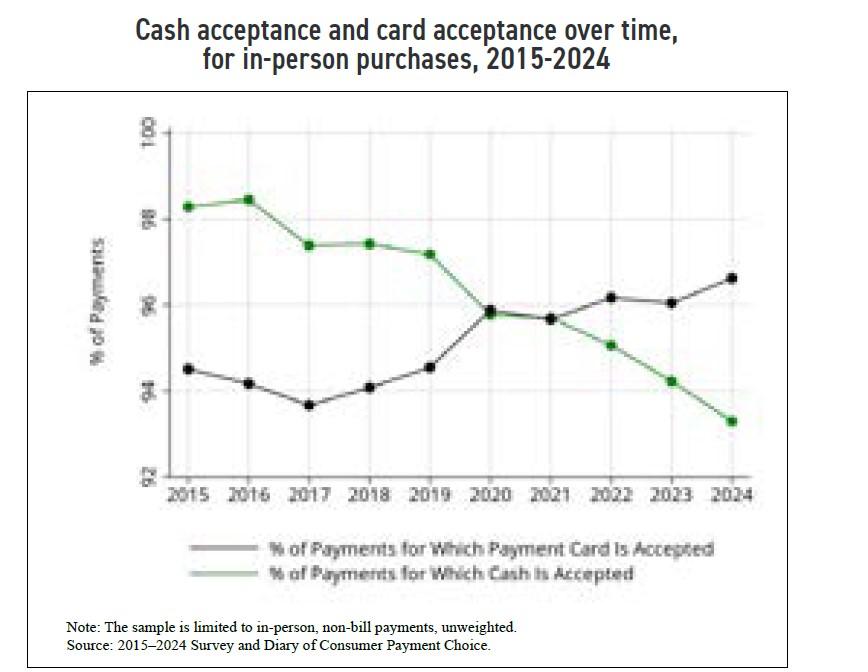

Refusal to accept a payment method remains rare but cash acceptance has decreased over time.

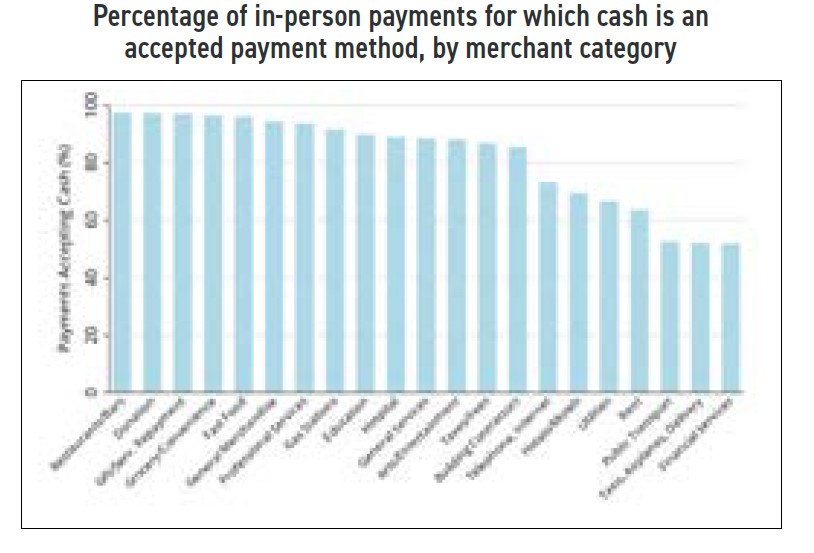

In addition, the refusal varies by merchant type. Cash acceptance is nearly universal at grocery and convenience stores and for purchases of food other than groceries (including restaurant meals), categories that together represent 57.6% of consumers’ in-person purchases.

Previous research has found that a large fraction of consumers prefers to use the same payment methods for all or most of their transactions.

There are several reasons for this observed behaviour:

When you read the findings, there is key message shouted from the roof tops. Legislation is needed to require cash acceptance if society wants cash to remain as a viable payment method.

What is this conclusion based on?

High transaction merchants want cash payments, but given surcharges and discounts won’t change behaviour, acceptance legislation is the ultimate safeguard to keep cash moving.

1 - Merchant Steering of Consumer Payment Choice Claire Greene. Oz Shy, and Joanna Stavins. Federal Reserve Bank of Atlanta Working Paper 2026-2.