The demand for cash is linked to GDP, deposit interest rates, demographics, financial inclusion, the size of the shadow economy and overseas demand. People respond to crises by hoarding cash. The Central Bank of the Republic of Turkey (CBRT) has used its October 2020 Methods of Payment Survey (MPS) to explore the role of financial literacy as a driver of cash usage 1.

The MPS carried out 2,400 face-to-face interviews and 1,537 of those filled out a payment diary from a Friday to a Monday. The interviews recorded socio-economic and demographic characteristics, payment method familiarity and the impact of COVID-19 on payment habits. A financial literacy score (FLS) was derived by asking a question about interest rates, inflation and risk diversification.

A right answer scored 1, a wrong answer -1 and if the respondent did not know, 0. A score of zero or less put people in the low category, 1 or 2 in the middle and 3 correct answers in the highest group. Only 7% of respondents got full marks.

There is no commonly accepted measure of financial literacy, but 16 countries have used this methodology. Only two countries had a lower score than Turkey. However, for interest rates Turkey was 9th. Interestingly gender, marital status and age made no difference to the scores. A higher income, education and living in one of the big five cities had a positive impact on scores, as did being unemployed, to the surprise of the report’s authors.

With cash usage reducing in many countries, there is evidence that new payment habits are forming. Central banks are neutral on payments in order to avoid excluding groups in society. Turkey’s MPS, its first, looked at patterns and determinants of the usage of payment instruments, finding a strong preference for cash. This finding makes it important that the CBRT understands the drivers of cash demand.

The theory in this area, based on work in Japan, says that as financial literacy increases, combined with access to cashless payments, the demand for transactional cash will fall, but not the demand for store of value cash. The household payment behaviour study in Poland showed that those with higher educational levels and higher material status used less cash. Canadian research found a negative correlation between cash on hand and financial literacy, but what about Turkey?

Cash holdings varied widely between 209 TL and 1,329 TL. Men tended to hold more than women, married people more than single, higher earners and employers more than others and the youngest and over 65 years old the least. The Mediterranean region held considerably more cash than other regions.

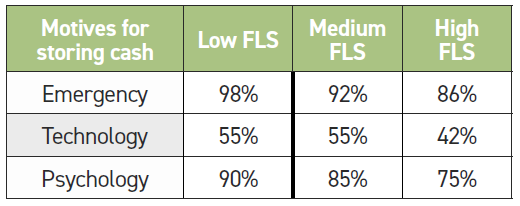

People with lower levels of financial literacy have high transactional demand for cash but low holdings of cash as a store of value. The paper raises the question whether the supply side fact that cash is always accepted in Turkey, while cards are not, may play a role in this.

The effect of financial literacy on non- transactional demand is higher than the reduction in transactional demand. Demographics and socio-economic factors are significant determinants of cash holdings of all types.

The conclusion was that people with higher FLSs need less cash on hand because they have a lower transactional demand. However, they hold more cash as a store of value, perhaps because they can afford to. The reason is not clear. Total cash holdings are higher for the financially literate because the difference in the cash held as a store of value is greater than the reduction in cash held for transactions.

A key finding, therefore, is that an increase in financial literacy will reduce cash usage at the point-of-sale (POS) but not the overall demand for cash.

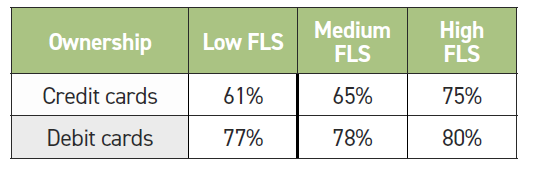

Card ownership is relatively high in Turkey.

In the study, card ownership is treated as a proxy of a readiness to pay cashless. It found that as financial literacy increased so did a willingness to pay with cards. It also found that during the pandemic those with higher levels of financial literacy were more likely to change their payment behaviour to use cards and to consciously avoid using cash.

The survey found that the financially literate are less concerned about the risk of technology failures stopping them paying.

Financial literacy was also a determinant of satisfaction when using a credit card, increasing users’ sense of well-being.

The MPS took place in October 2020 when the pandemic was having a significant impact. Given this was the first MPS there is no point of comparison. Were the levels of cash held for transactions lower and the store of value cash holdings higher as a response to the pandemic? This is certainly true in other countries.

The survey tested this and found that 23% or respondents were avoiding cash because of the pandemic. Cash in circulation rose 50% in Turkey during the pandemic and this must have been as a store of value.

As in other countries, those with lower levels of financial literacy did not increase their contactless payments as much as the other groups. Although card ownership is relatively high, perhaps this group had fewer alternatives.

1 - Working paper 22/02. Financial literacy and cash holdings in Turkey. Mustafa Recep Bilici, Saygın Çevi.