In 2023 in Canada digital payments accounted for 87% of total payment volume. Their uptake is only likely to rise as new ways of payment are invented. On top of open banking, faster payments, variable recurring payments, digital tokens, blockchain-based infrastructure etc. we can already see use cases build around programmability, possibly machine-to-machine payments driven by Artificial Intelligence (AI) and more.

A new Bank of Canada (BOC) paper on the costs of electronic retail payment networks has looked at how you balance out the benefits of multiple systems in one payments ecosystem and the fragmentation of volume and the replication of large fixed costs, which will raise the average cost of transactions 1.

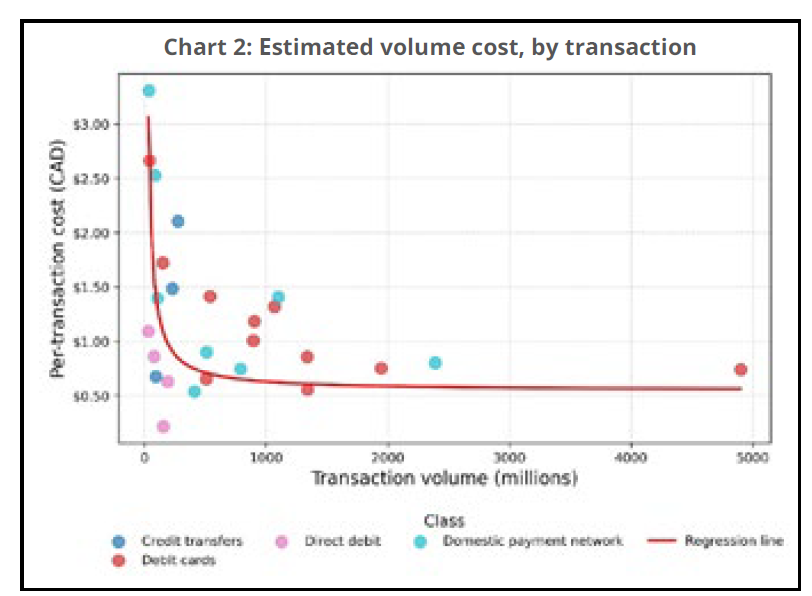

The paper seeks to understand the transaction volumes required for each system to reach the economies of scale where the average cost is minimised. To answer this, the paper made an estimate for the cost curve of the average electronic funds transfer (EFT) system and how the average cost declines with volume. This is needed for cost-benefit analyses, fee setting, benchmarking and justifying investment in new payment systems such as Canada’s Real Time Rail (RTR).

The paper found that the cost function decreases. Perhaps unsurprisingly, the shape of the decrease is convex in line with total transaction volume, reflecting the economies of scale in payment systems. There is a steep initial decline in per-transaction cost as transaction volume increases, suggesting that scale efficiencies emerge rapidly even at relatively low levels of usage.

Estimated volume cost, by transaction.

The estimated total fixed cost is approximately C$82 million per year, expressed in 2025 Canadian dollars, while the per-transaction cost is estimated at C$0.55. This result is consistent with evidence that electronic payment instruments (eg. information technology systems and card/point-of-sale terminals) have high fixed costs but comparatively low variable costs. Overall, the results point to declining average costs as volume increases.

EFT systems are networks of computer-based payment instruments that enable the transfer of funds between bank accounts, either within one institution or across institutions. Payments ecosystems are complex and interconnected patchworks of EFT systems. This complexity somewhat blurs the conceptual boundary between different payment instruments or forms.

To give a hint of the complexity, consider two payments initiated through distinct instruments, such as a credit transfer and a card payment. They may end up being cleared and settled on an underlying system such as a deferred net settlement system, a real-time gross settlement system or a fast payment system. Canada is about to introduce its fast payments system, the RTR.

New private payment rails for stablecoins and other blockchain-based infrastructure are coming on-line and need to work with existing systems. Evidence from Canada’s transition from its Large Value Transfer System to Lynx and academic research shows that adding new payment rails will shift volumes away from existing systems, with the magnitude of this substitution being highly sensitive to certain policy levers such as value caps and participation rules.

Ideally, each EFT system in an ecosystem should operate at efficient scale, with volumes high enough that their average cost lies very close to their respective marginal cost. If introducing a new EFT pulls transaction volumes from existing rails and pushes each rail down its average-cost curve, it will raise the average cost requiring fees to rise to cover these higher unit costs. If this leads to the effective price of payments across systems rising above the socially efficient level, the result would be a reduction in transaction volume relative to the optimum and the creation of a deadweight loss.

The paper posits that because the Canadian EFT system already processes high transaction volumes, it is already well within the flat part of the average-cost curve. Even if volumes were split across an additional system, each rail should remain close to efficient scale, with the average cost only slightly above the marginal cost. Purely in terms of cost-efficiency, so long as current transaction volumes were evenly distributed across all systems, Canada’s payments ecosystem could support several additional systems operating at efficient scale.

The paper looks at what will happen when the RTR comes on-line. It found that if projected usage exceeds the one-billion threshold, steady-state average costs should be close to the plateau.

Inevitably such as study comes with some caveats: