Guillaume Lepecq, Chair of Cash Essentials, and Matt Sykes, from the CPT Group, have written a paper about the business model of Automated Teller Machines (ATMs). Their conclusion? Circumstances have changed, and ATM business models need rethinking 1.

Ajay Banga, who was CEO of Mastercard until 2021, said at the end of his time at Mastercard, ‘I think cashless, actually, is something we’re not going to get to, and we probably shouldn’t’. This comment reflects a change of mood that is increasingly apparent, that cash has a unique value and needs to be sustained.

Sadly this mood is in part driven by a visible decline in cash use. The paper puts this down not to a lack of demand for cash, but a supply-side problem, particularly the sustainability of ATM business models.

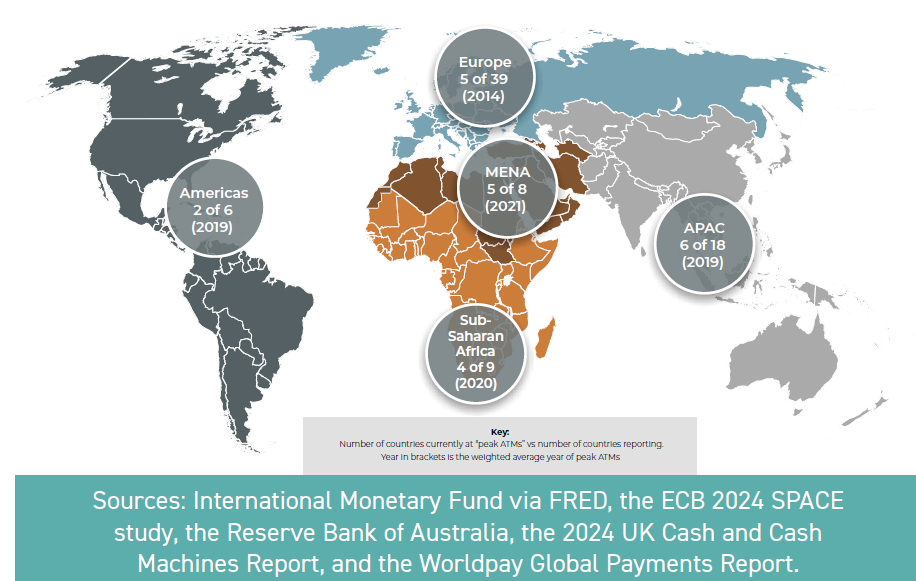

The paper states that ATMs are the single most important channel for delivering cash to the public across almost every market, with some 50-100 billion ATM transactions globally each year. However, ATM machine numbers are declining in more and more countries, and we are, it says, beyond ‘peak ATMs’.

In the chart of the countries at peak ATM and average year of peak ATMs in each region, only the Middle East and North Africa region had a majority of reporting countries where ATM fleets were still growing.

Some people suggest that alternative cash disbursement methods, such as branch and post office withdrawals, cashback at retail stores, and cash-in-shop services, could eventually replace ATMs.

The paper argues that, despite their convenience in specific scenarios, these alternatives remain niche solutions rather than viable replacements for ATMs. While they can complement cash distribution, they lack the scalability, universality, privacy and efficiency of ATMs. Their limited adoption, inconsistent business models, and inability to match the reliability of ATMs make them unsuitable as a primary cash access channel.

The current system is plagued by a lack of transparency, inconsistent fee structures, and a fundamental disconnect between the fees charged and the actual costs of operating ATMs.

ATM operators are essentially volume takers and price takers. This forces the ATM operator toward an often binary decision: keep an ATM in operation or remove it. Bank-operated or owned ATMs have to consider a range of factors – customer service, access and complaints; community service; overall network provision; brand visibility – in deciding whether to close an ATM, which can result in longer support for commercially unviable locations.

However, if there is a high proportion of ATMs which are independent and whose operators’ business is based on the commercial viability and success of the ATM fleet, which is a derivation of the viability of each individual ATM, then falling volumes will lead to a rapid reduction in ATM numbers.

The inception of ATM interchange was based on sound economic principles – to promote usage and access. However, as the cash and payments landscape has evolved, there is an argument that interchange is now doing the opposite of its original intent, and that both regulated models around interchange and purely market-driven interchange settings are problematic for consumer interests, ATM operator viability, and more broadly access to cash.

Moving forward, the key challenge for regulators and card schemes is to balance the interests of the various stakeholders: ensuring fair compensation for ATM owners, managing costs for issuing banks, and maintaining reasonable affordability for the end consumer. Interchange settings are in need of review.

The paper lists detailed recommendations for policy makers under different heading. These include:

1.Reform interchange fee structures

2.Public sector intervention

3.Encourage competition and innovation

4.Strengthen monitoring and resilience

5.Clarify regulatory mandates

6.Foster international cooperation.

The paper also suggests three concrete next steps for policy makers to take – creating a task force of interested parties, piloting reforms in high-risk areas, and monitoring and adapting to the impact of policies and evolving consumer needs and technological developments.

While this paper details suggested next steps for policymakers and offers a detailed overview of where ATMs are, the challenges they face and wide range of options for policy makers and the wider ATM industry to consider, it is also a call to action.

Action is needed now in line with the detailed recommendations and next steps in the paper if cash is to be preserved, economic resilience strengthened and the future of ATMs secured through innovation so that they remain relevant alongside digital payments.