The Swiss National Bank (SNB) runs a number of annual surveys to understand payment trends over time and what is happening now. The latest is the 2025 survey of payment methods of 2,000 private individuals, consisting of a questionnaire and the keeping of a payment diary for a seven day period 1.

Key findings are:

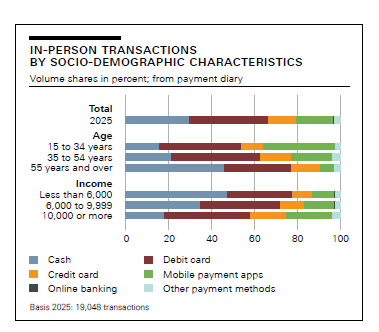

■At the point of sale (POS), payment methods have only changed a little since 2024, with debit cards used most frequently, followed by cash. Debit cards are used for 37% of in-person transactions, cash for 30%.

Since 2020 the volume share of cash has declined by 17 percentage points among respondents below the age of 55, and 13 percentage points for those aged 55 and over.

People with lower incomes used cash more frequently in 2025 than in 2024 for payments between private individuals, up from 55% to 62%. 1534 year olds made payments between private individuals at the lowest level, 22%, compared with 35% and 67% for 35-54 year olds and those 55 and over, respectively.

Cash is mostly used for payments at small retailers, as well as for services outside the home and when eating and drinking out.

While the ownership of cryptocurrencies and stablecoins has risen year on year, for payments, only 0.4% use them and so they are, effectively, irrelevant.

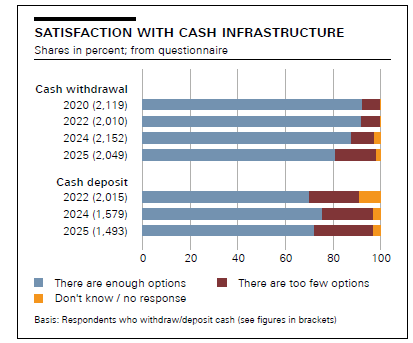

17% of respondents say there are too few access points, compared with 10% in 2024. SNB attributes this decrease in satisfaction to the fact that the number of ATMs – the most frequently used cash access point – have fallen by around 5% since the last survey. 25% of respondents are dissatisfied with the options available for depositing cash.

The majority of respondents go to their preferred cash access point on foot or by car, while just 9% use public transport. A total of 46% report that it takes very little time to reach the closest cash access point, compared with 52% in 2024. On average, respondents consider 12 minutes to be acceptable.

The percentage of people who regard holding cash at home, or in a safe deposit box, has increased steadily since 2020, and it is now well over half of respondents.

89% of respondents carry cash in their wallets, while the percentage keeping cash at home or in a safety deposit box has hardly changed since 2022, being 69% in 2025. Just under two-thirds hold cash to cover everyday expenses. One-third have a cash reserve at home that is not intended for everyday expenses.

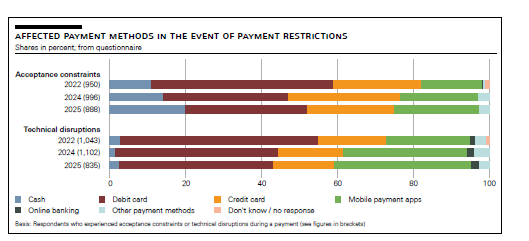

For the survey period, around half of the respondents experienced at least one situation in which a method of payment was not accepted or not welcomed by a retailer or service provider. A difference with previous surveys is that such situations more often resulted in the payment not being completed.

There has been a reduction in the number of situations in which technical disruptions prevented payment with the preferred payment method or in which the payment could not be completed – fewer than half of the respondents experienced a technical disruption.

While the payment method most affected by restrictions was the debit card, cash was mentioned more frequently than in previous years. Restrictions were most often experienced at festivals, concerts or fairs (46%) and when eating and drinking out (31%).

Despite this, satisfaction with cash acceptance remains very high, with 98% being satisfied or mostly satisfied. In around half of the cases of acceptance constraints or technical disruptions, cash was used as an alternative to complete the payment.

More respondents suffered financial losses in connection with the use of cashless payment methods (7%) than with cash (4%).

For cash, 2% reported that cash was stolen from them and 2% that they lost it. In the case of cashless payment methods, debit and credit cards are most frequently affected.

In most cases, the financial damage suffered is less than CHF 200 ($256).

The average amount lost was higher for cashless payment methods than for cash.

For cash most losses were for CHF 50 or less (45%) with losses of CHF 50-200 being about 35%. The figures for cashless payments were 25% for losses of CHF 50 or less and 40% being CHF 50-200.

While cash usage looks stable, early indicators around access and acceptance indicate cash is under pressure. Cash holdings and the wish for cash to remain reflect a deeply pro-cash culture in the country, although the payment behaviour of the young also indicates future change.