Schroders, a global asset management and wealth manager, has published a perspective piece, ‘Stablecoins: what they mean for the future of money’.

It explains and gives context about stablecoins, going as far as suggesting Central Bank Digital Currencies (CBDCs) are also a form of stablecoin. At the heart of the paper is the requirement for good regulation to unleash the full potential of stablecoins.

Financial volatility can be regarded as how much an assets value swings around the assets average price. In the US S+P 500 equities move plus or minus 21% and US grade investment bonds move 5% around their average price. In contrast Bitcoin has moved 85.15% since February 2018. It was suggested that as Bitcoin became more mature its volatility would decline, but this is not the case.

Stablecoins are different from cryptocurrencies because their value comes from their peg to an asset. Stablecoins claim to be digital currency because of how they work through digital wallets.

This means they can be, effectively, digital pocket change held in digital wallets rather than in bank accounts. Unlike today’s bank reserves, stablecoins are available to individuals. The underlying technology is blockchain that holds a digital ledger of transactions.

Advocates of stablecoins claim that they offer all the benefits of physical cash and more – transparency, security and immutability (the ledger can’t be changed). The transaction mechanism through digital wallets offers fast transactions, low fees, programmability and privacy. All this, depending on the reserving mechanism, without the volatility of cryptocurrency.

They must be doing something right given that today US dollar denominated stablecoins have a market capitalisation of $155 billion, achieved in only a few years.

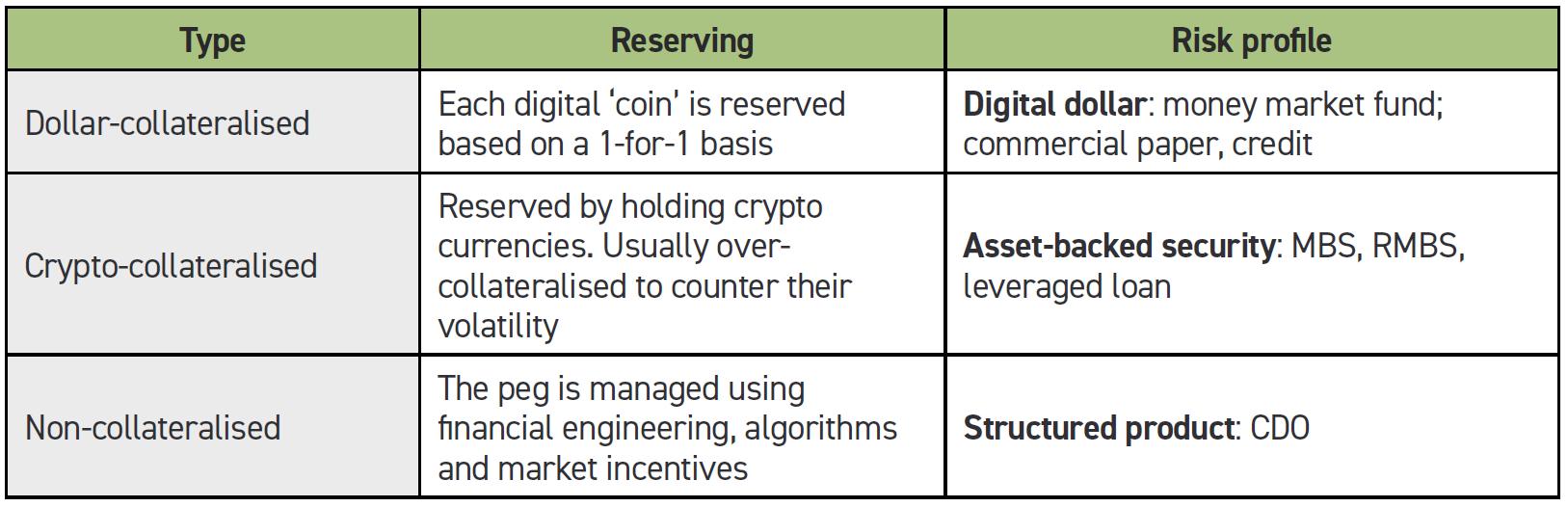

Schroders suggests there are three types of stablecoin with different abilities to deliver scale, stability and different levels of decentralisation. These characteristics trade-off across the different types bringing their own risk profile.

The three types are described in the table.

The value of Bitcoin is determined primarily by market demand, but also by its cost of creation. The value of stablecoins comes from their peg to an asset. Fully dollar- collateralised stablecoins operate in a similar way to money market funds. They have pegs that are backed by reserves of US Treasuries, certificates of deposit, commercial paper and corporate and municipal bonds.

The reserves of some projects have been questioned, for example in 2021 Tether was found to have 50% of its reserves in the form of commercial papers. This mix was regarded as representing unwanted credit risk.

In May 2022 UST, an algorithm stablecoin, collapsed, leading to a loss of $40 billion. Of the three types, this non-collateralised version of a stablecoin is unlikely to be accepted by regulators. In contrast during the recent Bitcoin hiatus, fiat backed stablecoins have maintained their peg values.

Ronald Reagan famously said: ‘if it moves, tax it. If it keeps moving, regulate it. And if it stops moving, subsidize it.’ Stablecoins have clearly passed through their initial stage because regulators around the world are now rushing to regulate them. Delivery of the potential benefits of stablecoins, and why they may be the future of money, requires regulation. Identity linked to wallets is the big challenge in all this.

Accelerated by result of recent events and the growing maturity of stablecoins, regulators around the world are developing prudential rules for how reserves should be managed to reduce counterparty risks.

This will introduce barriers to entry to new players, but regulation is necessary for stablecoins to fulfil their potential.

Schroders regard CBDCs as a form of public stablecoin. The issue for a public stablecoin is the risk of bank disintermediation that they introduce. A regulatory challenge talked about in the context of CBDCs is overseas holdings of them. There is already nothing to stop stablecoins existing irrespective of a US regulator, just as the Eurodollar banking system operates today.

The list of benefits starts with making the transfer of money from your bank onto an exchange so you can buy a cryptocurrency efficient and easy.

It goes on to the ability to hold stablecoins in digital wallets on phones without going through the banking system. This allows people to make payments, including sending currency globally instantly and, essentially, free of charge. No more 3% fees, or more, and long delays in settlements.

More competition in domestic payment markets should also drive down card fees.

For those into gaming, stablecoins offer an easier online payment solution than fiat money. Gaming is changing so that players own objects and characters within games, rather than companies, and so payment is increasing in importance.

Programmable money using smart contracts is possible with stablecoins. Schroders gives examples of governments using this capability to target fiscal expenditure, enable tiered interest rates for selected groups and to make direct payments to households.

While stablecoins bring similar risks of bank disintermediation and ‘dollarisation’ as a CBDC, the impact on foreign exchange trading would be to allow markets to be made between non-traditional currency pairs, bypassing major institutions. This would support emerging markets.

Finally, digital wallets would allow financial products to become open-sourced and programmable. This offers opportunities to give the unbanked access to financial products.

If stablecoins can deliver all or some of these, then so can CBDCs. Which focuses the mind on whether CBDCs are necessary and what they can do that well regulated stablecoins can’t.